LuxAlgo Backtesting System

caution

Backtests are not indicative of future results. Backtesting strategies on synthetic data does not return representative results of a strategy. Backtests should be performed on charts returning real closing prices. See here for more information.

CFTC Rule 4.41 - Hypothetical or Simulated performance results have certain limitations, unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not been executed, the results may have under-or-over compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profit or losses similar to those shown.

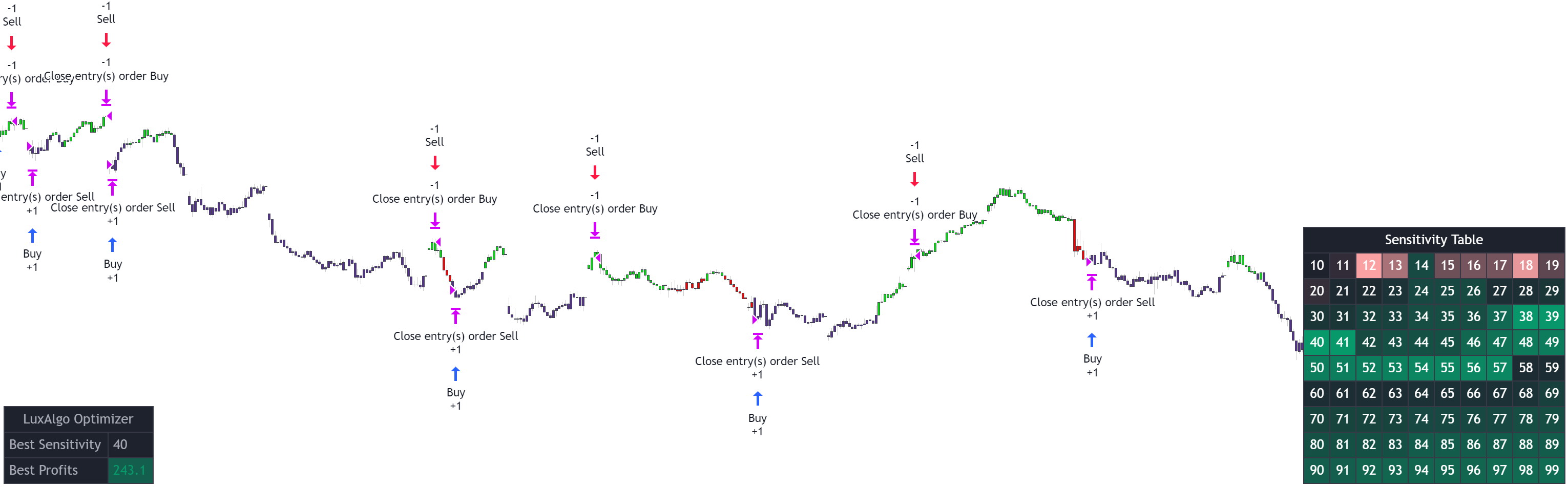

The LuxAlgo Backtesting System is an advanced script in closed beta that allows users to perform backtests from confirmation signals. Many options are included to provide more complete and diverse backtestings to the user, each core component of the scripts are described in the following pages:

»Entry Rules»Take Profit & Stop Loss»Exit Conditions»Settings Optimization»Alerts»Changelogcaution

The LuxAlgo Backtesting System is currently in a closed BETA and is only available to beta testers. Beta testers may not receive frequent updates.